He was the topper of my class. At 25, he was drowning in debt.

I taught for 14 years. And I watched my smartest students walk into the real world and fall apart over the one subject we never taught them: money. This is what I learned — and what I finally did about it.

I've been a teacher for most of my adult life. In that time you learn to spot the bright ones early. The students who sit a little straighter, finish first, ask the question you didn't expect.

Avik was one of those.

He was the kind of student every teacher quietly hopes for. First rank, year after year. The parents everyone envied. When he left for college, I remember thinking, that one's going to be just fine.

I was wrong. And it took me years to understand why.

Here's what I didn't expect

I ran into Avik's mother about eleven years later.

Avik had done everything right on paper. Good college, good marks, a real job with a real salary. But the moment that salary started landing in his account, something none of us had prepared him for began to unravel.

A credit card he didn't understand. Then a second one to cover the first. A "buy now, pay later" habit that quietly became a monthly hole. An EMI on a phone, an EMI on a laptop, an app-based loan he took at 3 a.m. because the money was just there.

By 25, my brightest student — the boy who could solve any equation I put on the board — was lying awake at night terrified of a number in a banking app. He earned well. He still had nothing. And he felt ashamed, as if it were a personal failing.

It wasn't. That's the part that haunted me.

We prepared him for everything except this

Here's what I couldn't stop thinking about.

In all my years of teaching, we had prepared Avik for everything except the thing he'd use every single day for the rest of his life. We drilled him on trigonometry, on the periodic table, on the dates of battles fought centuries ago. We never spent one honest hour teaching him what a loan actually costs, how a credit card really works, or why saving early quietly changes an entire life.

We didn't fail him because he wasn't smart. We failed him because nobody had taught us to teach this.

And I started to wonder: how many Avik's were out there?

So I went looking for the answer

What I found genuinely disturbed me.

According to the Standard & Poor's Global Financial Literacy Survey, one of the largest studies of its kind ever done, only about 24% of Indian adults are financially literate. Roughly three out of four grown adults in this country don't confidently understand basic ideas like interest, inflation, or spreading out risk.

Then I saw the number that truly stopped me. India ranks below Pakistan, where the figure is around 26%. We are behind our neighbour on the one skill our children need most.

And why wouldn't we be? Personal finance still isn't a required, examined subject in most Indian schools. There's no board exam for it. No tuition class for it. We have quietly decided that our children will figure out money the way we did: alone, late, and the hard way, through mistakes that can cost them a decade of their lives.

Avik wasn't an exception. Avik was the rule.

I couldn't change the system, but I could do something

I couldn't rewrite the syllabus. I couldn't rewrite government policy. But I could not keep sending bright kids into the world financially blind and call it teaching.

So I started looking for something simple, age-appropriate, and real enough that a 12-year-old and a 17-year-old could each learn what they were ready for. That search is how I found the National Finance Olympiad Personal Finance Handbooks.

What happened when I started handing them out

I'll be honest. I didn't wait for a school committee or an official program. I started buying them myself and handing them to my students, grade by grade.

The change was not loud, but it was unmistakable. Kids who used to think money was just "something adults worry about" started asking sharp questions. What's the difference between saving and investing? Why is a credit card dangerous if you only pay the minimum? Is this "guaranteed double your money" thing a scam?

These were the exact questions Avik was never taught to ask — and here were 13-year-olds asking them out loud, before the mistakes, not after.

That's when I understood. This isn't about turning children into accountants. It's about making sure that when the first salary lands, they're the ones in control of it, instead of the other way around.

If you're a parent, this is for you

I want to say the thing I wish someone had said to me before I met Avik's mother that day.

Your child's marks will not protect them from a debt trap. Their degree will not teach them to save. The world your child is walking into — loan apps, endless EMIs, credit cards handed out like sweets, "tips" from strangers online — is designed to profit from exactly what we never taught them.

You can close that gap. And you don't need to be good with money yourself to do it. Many of us aren't, because nobody taught us either. You just need to put the right thing in their hands early, while it's still a lesson and not an expensive scar.

What the handbooks actually are

They're written grade by grade, so a younger child learns money in words they can actually grasp, and an older one learns what they'll genuinely need the day their first paycheck arrives. No jargon. No lectures. Just the real-world money skills school skips: saving, budgeting, smart spending, earning, and spotting the traps.

And here's the quiet bonus: most parents tell me they end up learning right alongside their child.

You won't be the first to do this

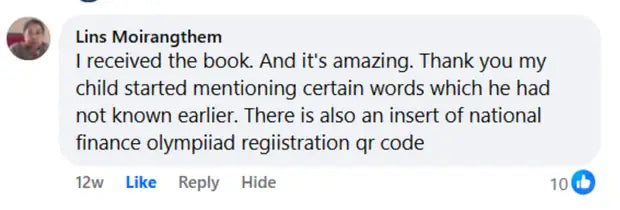

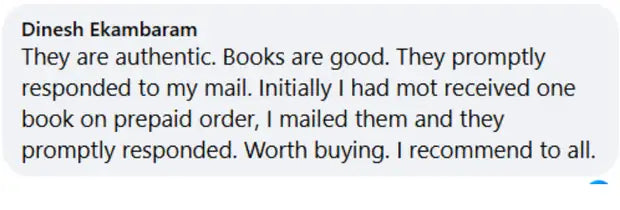

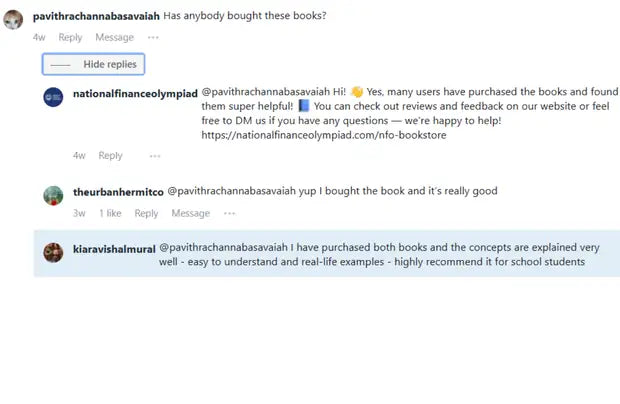

Today these handbooks are already trusted by:

"Is my child too young for this?"

The money habits that decide whether an adult saves or sinks form far earlier than most of us believe. The best time to teach a child about money is not after their first bad decision at 25. It's now, while it still costs them nothing to learn.

Don't wait for the school system

It won't teach this in time.

Give your child the one advantage a report card can't, before the world teaches them the hard way, the way it taught Avik.

P.S. I still think about Avik. He's doing better now. He taught himself, painfully, in his late twenties, everything we should have given him at twelve. Your child doesn't have to learn it that way. That's the whole point.

Personal Finance Handbook